Why manual document workflows quietly inflate expense, increase risk, and slow growth and how insurers can modernize without ripping and replacing core systems?

Executive Summary

- Claims delays and fragmented communications directly impact customer loyalty: when the digital claims experience is rated “poor” or “just OK,” 52% of customers say they are likely to leave; that drops to 4% when the experience is “excellent” or “perfect.”

- Cycle time is still a major drag: J.D. Power reports the average claimant does not receive final payment until ~44 days after first notice of loss (2025).

- Regulators are enforcing documentation and reporting requirements: NYDFS concluded a multi-year investigation resulting in 37 consent orders and $20.4M in fines for untimely reporting.

What Is the Real Cost of Not Automating Insurance Forms Processes?

Many insurers still believe that sticking with manual workflows is the cheaper option, especially when automation is perceived as complex, disruptive, or resource-intensive. But recent industry data tells a different story.

In 2025, AI-enabled insurers reduced claims resolution times by up to 75% and cut processing costs by 30–40%, while the average claim cycle time across the industry stretched to 44 days, the longest on record. The gap between leaders and laggards has never been wider.

In this article, we’ll explore the hidden and increasingly visible costs of delaying insurance document automation, why those costs are accelerating, and what insurers can do now to regain control.

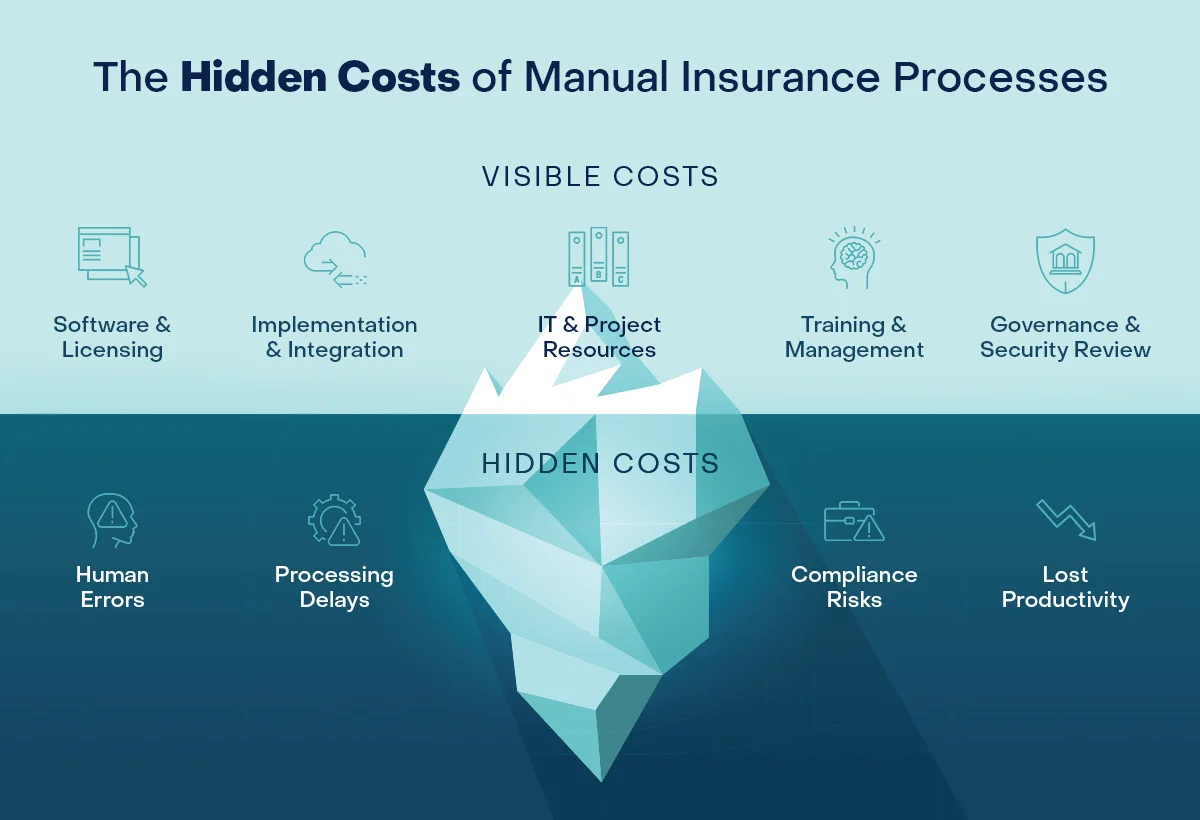

The Real Cost Isn’t “Paper.” It’s the Work Around It.

Most insurers don’t lose money because a PDF exists. They lose money because people must repeatedly correct, re-key, route, reconcile, and re-issue documents across systems. Those “small” touches compound into three predictable cost drains:

1) Rework from Human Error

Manual data entry and document assembly increase missing fields, incorrect values, and inconsistent wording. The downstream impact shows up as adjuster rework, delays, customer callbacks, and avoidable disputes.

2) Cycle Time (and the Churn It Creates)

Customer tolerance for waiting is shrinking, particularly in claims. In property insurance, J.D. Power found that the average time from first notice of loss to final payment exceeded 44 days in 2025, the longest since the study began. Those delays don’t stay operational for long. As cycle time stretches and communication breaks down, customer loyalty erodes. Study shows that 52% of policyholders are likely to leave when the digital claims experience is poor or just acceptable, compared to only 4% when it is excellent.

3) Compliance Exposure

When documents are inconsistent, missing, or filed late, insurers absorb more than audit pain. They absorb penalties, remediation work, and reputational risk. For example, NYDFS issued 37 consent orders totaling $20.4M in fines tied to untimely reporting of insured/uninsured vehicles, an operational issues rooted in reporting and process discipline.

Where Money Leaks (Even When No One Is Tracking It)

Claims Intake and Customer Communications

Every claim triggers a chain of document-driven touchpoints; acknowledgements, letters, evidence requests, estimates, settlement summaries, and status updates. When these are assembled manually, cycle time grows and customers are forced to call for clarity and updates. In practice, proactive digital updates are delivered only 22% of the time, creating unnecessary inbound volume and frustration.

Underwriting and Policy Issuance

Underwriting remains one of the most document-intensive functions in insurance, yet much of the work still revolves around non-core administrative activity. It’s a labor-intensive task of collecting information, validating inputs, assembling documents, managing exceptions, and coordinating approvals across systems. These manual steps slow policy issuance, increase operational cost, and limit underwriters’ ability to focus on risk evaluation and pricing decisions.

While insurers clearly recognize the need to improve efficiency, execution has lagged. A late-2024 survey of more than 240 insurance executives found that improving financial performance and operational efficiency is a top priority for both underwriting and claims teams. At the same time, the study revealed that most organizations are still struggling to scale automation beyond pilots, leaving document-heavy workflows largely unchanged and the expected gains unrealized.

Regulatory Reporting and Audit Readiness

Manual file handling makes it harder to prove “who changed what, when, and why.” Automated document workflows create standardized outputs, retention policies, and audit trails that reduce remediation effort when regulators ask questions.

Why “Later” Is Too Late – The Cost of Delaying Automation

Delaying automation doesn’t hold costs steady, it compounds them.

As document volumes increase, regulations evolve, and customer expectations shift toward real-time, digital-first experiences, manual processes become more expensive to sustain and more difficult to unwind. What starts as manageable inefficiency quickly scales into operational drag.

The cost isn’t just labor. It’s hidden in slower time-to-revenue, rework, error correction, and missed opportunities. Every delayed quote, policy, or claim introduces friction into the customer journey and friction directly impacts conversion, retention, and lifetime value.

At the same time, risk exposure grows. Manual document processes increase the likelihood of inconsistent language, version control issues, and audit gaps. In regulated industries like insurance, that’s not just inefficient it’s a liability.

Meanwhile, AI-driven insurtechs and digital-first competitors are resetting the benchmark. They’re underwriting faster, processing claims more efficiently, and delivering seamless, self-service experiences at scale. This isn’t incremental improvement, it’s structural advantage.

The longer automation is delayed, the harder and more expensive it becomes to implement. More processes, more exceptions, and more technical debt accumulate. Turning what could have been a targeted initiative into a large-scale transformation effort. Automation is no longer a future optimization. It’s a present-day requirement to control costs, reduce risk, and remain competitive.

Case Study – What Happens When Insurers Automate

GroupHEALTH Benefit Solutions, a provider of health benefits across Canada, struggled with outdated, paper-based enrollment processes. These outdated processes led to costly errors, poor customer experiences, and low optional coverage sales.

They partnered with Experlogix and the results were dramatic:

- 5,000% increase in optional coverage sales thanks to embedded explainer videos and real-time personalization

- 20–25% reduction in enrollment management costs

- Elimination of manual data entry errors (e.g., misspelled names that previously caused drug coverage denials)

- Faster processing during open enrollment and better client satisfaction

Experlogix for Insurance Companies

Experlogix is built for industries with complex document workflows, like insurance, where legacy systems, compliance demands, and limited IT bandwidth often slow down transformation. It is designed to remove that friction from day one.

There is no “rip-and-replace” required when it comes to your legacy systems. Experlogix integrates with your legacy systems, like core insurance platforms, CRMs, and ERPs. Teams can move fast without disruption.